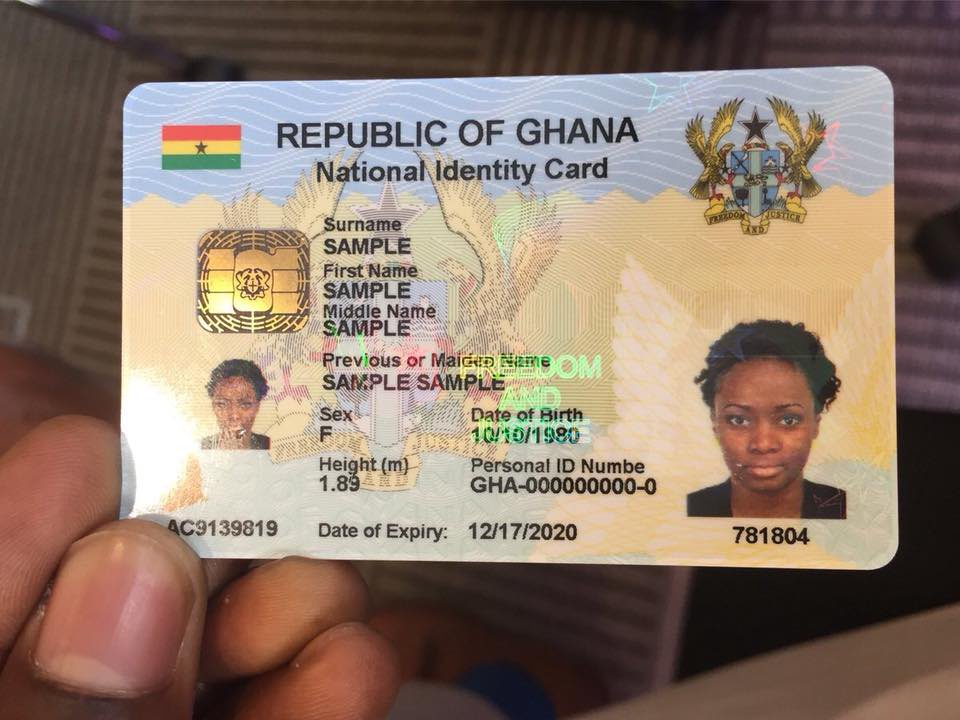

Ghana has taken a major step toward financial inclusion by enabling payments through its national identification system. The National Identification Authority has introduced a digital wallet feature on the Ghana Card, allowing citizens to use their ID for financial transactions.

The Ghana Card, already used for services such as SIM registration and passport applications, now supports payments at ATMs, in stores, and online. Users can also make international transactions across more than 200 countries and access additional services such as insurance and emergency support.

To activate the wallet, cardholders can use the MyCitizens App or dial a short code on their mobile devices.

Driving Financial Inclusion Through Identity

The introduction of a digital wallet addresses a key challenge in Ghana’s financial system. Credit card usage remains extremely low, with penetration estimated at just 0.6 percent in 2024.

By embedding financial services into a widely held national ID, the government aims to reduce barriers to access. This approach allows more citizens to participate in the financial system without requiring traditional banking infrastructure.

ALSO READ: Visa Launches Tools to Reduce Payment Disputes

The Ghana Card was originally designed with three core functions in mind: identity, passport, and payments. The identity system is already active, while the e passport feature launched in 2022 and gained international recognition.

The addition of a wallet completes this vision, turning the card into a multifunctional tool for both identification and financial activity.

A Unified Platform for Financial Services

Unlike traditional payment systems, the Ghana Card wallet is not controlled by a single financial institution. Instead, it operates as a unified platform that integrates multiple banks.

This structure allows users to access financial services without being tied to one provider. It also creates opportunities for broader participation across the banking sector.

The system could simplify transactions and reduce dependency on external payment networks, particularly in regions with limited access to traditional banking services.

Potential Impact on Payments Ecosystem

If widely adopted, Ghana’s model could reshape how payments are delivered across Africa. Identity based financial systems may offer an alternative to global card networks such as Visa and Mastercard.

By linking identity directly to financial services, governments can create more inclusive and efficient payment systems. This approach may also reduce transaction costs and improve accessibility for underserved populations.

ALSO READ: Visa Warns AI Alone Cannot Stop Rising Financial Scams

In addition, the integration of financial services with national IDs can support digital transformation efforts and strengthen economic participation.

Expanding Use Cases Beyond Payments

The Ghana Card wallet may extend beyond everyday transactions. The National Identification Authority has explored potential partnerships to support activities such as gold trading and tokenized transactions.

While these features have not yet been fully implemented, they highlight the broader vision for the platform. The goal is to create a digital ecosystem where identity, finance, and economic activity are interconnected.

Challenges and Considerations

Despite its potential, the system faces several challenges. Adoption will depend on user trust, infrastructure readiness, and integration with existing financial services.

Security and data protection will also play a critical role. As identity and financial data converge, ensuring privacy and safeguarding user information becomes essential.

Additionally, collaboration between government agencies, banks, and technology providers will be necessary to maintain system reliability and scalability.

Future Outlook for Identity Based Payments

Ghana’s initiative represents a shift toward identity driven financial systems. By combining identification and payments, the country is testing a model that could influence other African markets.

If successful, this approach may accelerate financial inclusion and redefine how digital payments operate in emerging economies.

The Ghana Card could become more than an identification tool. It may evolve into a central platform for accessing financial services, supporting economic growth, and enabling broader participation in the digital economy.

MORE STORIES:

Unlocking the Power of Digital Agriculture in Africa

Unlocking the Power of Digital Agriculture in Africa

Visa Launches Tools to Reduce Payment Disputes

Visa Launches Tools to Reduce Payment Disputes

President Kagame Pushes for Social Media Monetization in Rwanda

President Kagame Pushes for Social Media Monetization in Rwanda

Engineer Introduces Device That Turns Any TV Into Smart TV

Engineer Introduces Device That Turns Any TV Into Smart TV

TikTok Faces Scrutiny for Not Adopting End to End Encryption

TikTok Faces Scrutiny for Not Adopting End to End Encryption

Education Evolution: From Obsolete Skills to AI-Ready Classrooms

Education Evolution: From Obsolete Skills to AI-Ready Classrooms

National Bank Reports Drop in Digital Payment Fraud Cases

National Bank Reports Drop in Digital Payment Fraud Cases

Google Pixel 10a Review: Small Tweaks, Same Reliable Formula

Google Pixel 10a Review: Small Tweaks, Same Reliable Formula

Meta and YouTube Face Historic Trial Over Allegedly Designing Addictive Platforms for Children

Meta and YouTube Face Historic Trial Over Allegedly Designing Addictive Platforms for Children

Google Expands Gemini 3.1 Pro Across Cloud and Enterprise

Google Expands Gemini 3.1 Pro Across Cloud and Enterprise

hacklink paneli,otomatik sistem En iyi sistem,kırık linke son!

hacklink satın al , hacklinktr en iyi hacklink paneli

canlı taraftarium24 izle hd kalite

hacklink satın al google 1. sıra hizmet googlede yüksel bet seo

Email: support@alo8.chat