AI Generated image

Mobile money users in Rwanda can reduce their risk of fraud by slowing down, checking transaction records and refusing to disclose confidential information when a caller or message demands urgent action. Many common scams depend on persuading the account holder to authorise a payment rather than directly breaking into the payment system.

An opinion article published by The New Times on 13 July 2026 by personal finance expert Lynnette Khalfani-Cox identifies several recurring methods. These include false claims about mistaken transfers, callers pretending to represent customer care, fake prize messages and urgent requests involving relatives.

The National Bank of Rwanda advises mobile money users to verify recipient details, protect their PINs and passwords, and report suspected fraud or cyberattacks promptly. Rwanda Investigation Bureau has also warned the public to be cautious when receiving sudden requests to transfer money, including requests appearing to come from known contacts.

KEY FACTS

- Check the actual mobile money balance and transaction history before responding to a claim that money was sent by mistake.

- Do not disclose a PIN, password or verification code to someone who calls or sends a message.

- Verify urgent financial requests by contacting the person or institution through a separately confirmed number.

- Avoid links sent through suspicious text messages, emails or social-media accounts.

- Report suspected fraud quickly to the mobile money provider and the relevant authorities.

HOW FALSE TRANSFER CLAIMS WORK

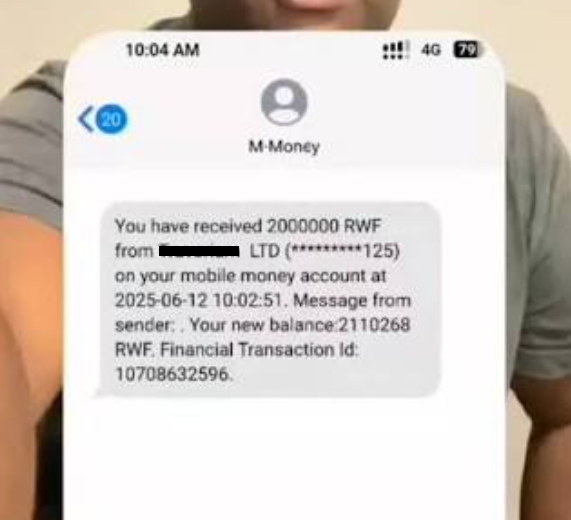

A person may call or send a message claiming to have transferred money to the wrong number. The caller may then ask the recipient to return it immediately.

Before taking any action, the account holder should inspect the official transaction notification, current balance and recent transaction history. A message written by the caller or a screenshot sent through a messaging application is not sufficient proof that money entered the account.

When an actual transfer appears to have been made incorrectly, the safest approach is to contact the financial service provider through its official customer-support channel. Users should not send money to another number simply because the caller gives urgent instructions.

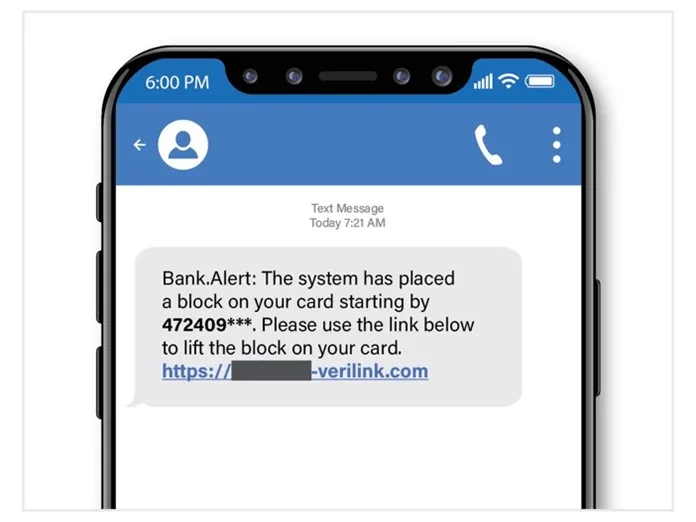

CALLERS POSING AS CUSTOMER-CARE STAFF

Another method involves someone claiming to work for a mobile network, bank or payment provider. The caller may say there is a failed transaction, blocked account, prize payment or technical problem that requires immediate action.

The fraudster may ask the user to disclose a PIN, read a verification code aloud, change account settings or enter a sequence of numbers. These requests can give the criminal information or authorisation needed to access the account or complete a transfer.

Airtel Rwanda advises users to keep their mobile money PIN secret and states that customers are not required to give it to an agent or company representative. BNR similarly requires consumers to safeguard their credentials and remain cautious about calls, messages and emails directing them to take actions on their accounts.

FAKE PRIZES AND SUSPICIOUS LINKS

Some messages tell users that they have won cash, airtime, a telephone or another reward. However, the supposed winner is then asked to pay a fee, enter a code or open a link before receiving the prize.

A legitimate promotion should be confirmed through the organisation’s official website, application, office or verified customer-care channel. Users should not rely on the telephone number or link included in the suspicious message itself.

BNR advises consumers not to respond to unknown links because they may be phishing attempts designed to obtain passwords, account details or other private information.

URGENT REQUESTS INVOLVING RELATIVES

Fraudsters may also claim that a relative or friend is sick, stranded, under arrest or facing another emergency. In some cases, the request may appear to come from a familiar telephone number or account.

The recipient should call the relative using a number already stored or independently confirmed. When possible, another family member should also be contacted before money is transferred.

RIB has specifically advised the public to be cautious about sudden mobile money requests that appear to come from people in their contact lists. This warning is important because the appearance of a familiar name or number does not prove that the request is genuine.

EVERYDAY STEPS THAT REDUCE THE RISK

Users should check the recipient’s name, telephone number and amount before approving any payment. They should also confirm that the transaction was completed before attempting it again, since repeated attempts may result in more than one transfer.

PINs and passwords should not be based on easily guessed information such as birthdays or simple number sequences. They should also be changed when there is reason to believe that another person has seen or obtained them.

Urgency should itself be treated as a warning sign. Pausing briefly gives the user time to inspect the account, contact the supposed sender and reach the provider through an official channel.

WHAT TO DO AFTER SUSPECTED FRAUD

A person who suspects that account information has been exposed should contact the financial service provider immediately. The user should explain what happened, request assistance and change the PIN or password where appropriate.

Messages, transaction references, telephone numbers and other relevant records should be preserved. They may assist the provider or investigators in tracing the incident.

Suspected criminal cases can be reported to Rwanda Investigation Bureau through its official reporting channels, including the toll-free number 166. BNR guidance also advises consumers to notify their provider or RIB immediately when they suspect fraud or a cyberattack.

Mobile money remains useful for everyday payments, transfers and other financial services. However, users should remember that an urgent message, professional-sounding caller or familiar telephone number is not proof that a request is genuine. Independent verification remains one of the strongest protections against fraud.

Credit: The New Times

MORE STORIES:

MTN Rwanda Returns to Profit in Q1 2026

MTN Rwanda Returns to Profit in Q1 2026

Rwanda Approves Cryptocurrency Regulation Law

Rwanda Approves Cryptocurrency Regulation Law

US Real-Time Payments Enter High Growth Phase

US Real-Time Payments Enter High Growth Phase

Why Google and AI Companies Are Fighting Search Manipulation

Why Google and AI Companies Are Fighting Search Manipulation

A Beginner’s Guide to Invest in Rwanda Stock Exchange

A Beginner’s Guide to Invest in Rwanda Stock Exchange

AI model risks: Regulators monitor Anthropic’s mythos over financial system concerns

AI model risks: Regulators monitor Anthropic’s mythos over financial system concerns

Your personal address is being sold online. Here is a tool that can help

Your personal address is being sold online. Here is a tool that can help

Visa Warns AI Alone Cannot Stop Rising Financial Scams

Visa Warns AI Alone Cannot Stop Rising Financial Scams

Ghana’s National ID cards can now make payments

Ghana’s National ID cards can now make payments

Taking Down “Quackers”: Inside a Global Dark Web Investigation

Taking Down “Quackers”: Inside a Global Dark Web Investigation